Discounted Cash Flow Valuation Method

Valuation is the analytical process of determining the current (or projected) worth of an asset or a company. There are many techniques used for doing a valuation. An analyst placing a value on a company looks at the business’s management, the composition of its capital structure, the prospect of future earnings, and the market value of its assets, among other metrics. There is one method that Analysts also place a value on an asset or investment using the cash inflows and outflows generated by the asset, called a Discounted Cash Flow (DCF) analysis.

This method estimates the value of an asset based on its expected future cash flows, which are discounted to the present value. This concept of discounting future money is commonly known as the time value of money. For instance, an asset that matures and pays $1 in one year is worth less than $1 today. The size of the discount is based on an opportunity cost of capital and it is expressed as a percentage or discount rate.

In finance theory, the amount of the opportunity cost is based on a relation between the risk and return of some sort of investment. Classic economic theory maintains that people are rational and averse to risk. They, therefore, need an incentive to accept risk. The incentive in finance comes in the form of higher expected returns after buying a risky asset. In other words, the more risky the investment, the more return investors want from that investment. Using the same example as above, assume the first investment opportunity is a government bond that will pay interest of 5% per year and the principal and interest payments are guaranteed by the government. Alternatively, the second investment opportunity is a bond issued by small company and that bond also pays annual interest of 5%. If given a choice between the two bonds, virtually all investors would buy the government bond rather than the small-firm bond because the first is less risky while paying the same interest rate as the riskier second bond. In this case, an investor has no incentive to buy the riskier second bond. Furthermore, in order to attract capital from investors, the small firm issuing the second bond must pay an interest rate higher than 5% that the government bond pays. Otherwise, no investor is likely to buy that bond and, therefore, the firm will be unable to raise capital. But by offering to pay an interest rate more than 5% the firm gives investors an incentive to buy a riskier bond.

For a valuation using the discounted cash flow method, one first estimates the future cash flows from the investment and then estimates a reasonable discount rate after considering the riskiness of those cash flows and interest rates in the capital markets. Next, one makes a calculation to compute the present value of the future cash flows.

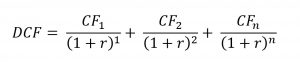

Discounted Cash Flow Formula

The discounted cash flow (DCF) formula is equal to the sum of the cash flow in each period divided by one plus the discount rate (WACC) raised to the power of the period number.

Here is the DCF formula:

Where:

CF = Cash Flow in the Period

r = the interest rate or discount rate

n = the period number

Analyzing the Components of the Formula

1. Cash Flow (CF) DCF Formula – Cash Flow

Cash Flow (CF) represents the free cash payments an investor receives in a given period for owning a given security (bonds, shares, etc.)

When building a financial model of a company, the CF is typically what’s known as unlevered free cash flow. When valuing a bond, the CF would be interest and or principal payments.

To learn more about the various types of cash flow, please read CFI’s cash flow guide.

2. Discount Rate (r) DCF Formula – Discount Rate

For business valuation purposes, the discount rate is typically a firm’s Weighted Average Cost of Capital (WACC). Investors use WACC because it represents the required rate of return that investors expect from investing in the company.

For a bond, the discount rate would be equal to the interest rate on the security.

3. Period Number (n) DCF Formula – Period

Each cash flow is associated with a time period. Common time periods are years, quarters or months. The time periods may be equal, or they may be different. If they’re different, they’re expressed as a decimal.

DCF Formula Used For?

The DCF formula is used to determine the value of a business or a security. It represents the value an investor would be willing to pay for an investment, given a required rate of return on their investment (the discount rate).

Examples of Uses for the DCF Formula:

To value an entire business

To value a project or investment within a company

To value a bond

To value shares in a company

To value an income producing property

To value the benefit of a cost-saving initiative at a company

To value anything that produces (or has an impact on) cash flow

Source :

[1] https://en.wikipedia.org/wiki/Valuation_(finance)

[2] https://www.investopedia.com/terms/v/valuation.asp

[3] https://corporatefinanceinstitute.com/resources/knowledge/valuation/dcf-formula-guide/

Thanks for great sharing Mr. Alun, but let me ask questions, how do you evaluate a fair value of a stock if the firm have nearly zero free cash flow? and which one is the best between including or excluding capital expenditure in counting discounted free cash flow to reflect stock’s intrinsic value?