What is Beta (β) in Finance: Medco International Energy Case

In the Capital Asset Pricing Model, Beta is used for calculate the expected return of an asset.Beta is a measure of the volatility, or systematic risk, of a security or a portfolio in comparison to the entire market or a benchmark. Beta is also known as the beta coefficient. A company with a higher beta has greater risk and also greater expected returns. The beta coefficient can be interpreted as follows:

- β =1 exactly as volatile as the market

- β >1 more volatile than the market

- β < 1 > 0 less volatile than the market

- β =0 uncorrelated to the market

- β <0 negatively correlated to the market

Calculating the Beta (β)

Beta, specifically, is the slope coefficient obtained through regression analysis of the stock return against the market return. More detail, Beta coefficient is tendencies of security return against the swing of market return. It is can be formulated by dividing the product of the covariance of the security’s returns and the benchmark’s returns by the product of the variance of the benchmark’s returns over a specified period. The equation of Beta formula is as follow:

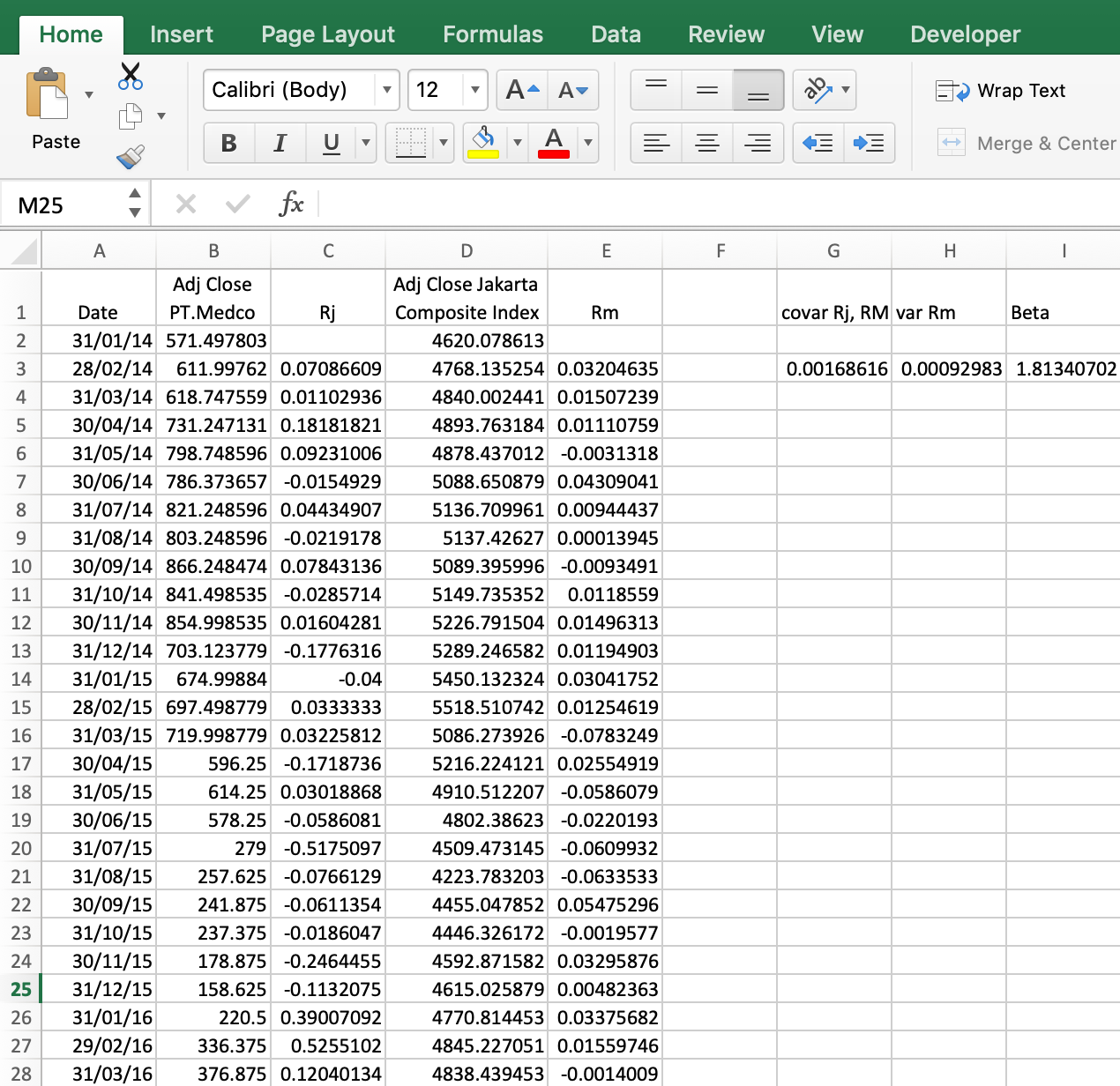

Beta (β) = Covariance (Rj,Rm)

Variance (Rm)

Where:

Covariance(Rj,Rm) = Covariance of asset and market

Variance(Rm) = Variance of market

Medco International Energy Beta

To calculate Beta coefficient of PT. Medco, we need to gather all the data first. The data can be obtain from https://finance.yahoo.com, the step for calculating Beta as follow:

- Obtain the monthly prices of the stock for five years (longer the period, the calculation will be more precise) from this link https://finance.yahoo.com/quote/MEDC.JK/history?p=MEDC.JK&.tsrc=fin-srch

- Obtain the monthly prices of the market index for five years from Jakarta composite Index where PT. Medco International energy listed, from this link https://finance.yahoo.com/quote/%5EJKSE/history?period1=1517567993&period2=1549103993&interval=1mo&filter=history&frequency=1mo

- Calculate the monthly returns of the stock

- Calculate the monthly returns of the market index

- Calculate the Covariance of Monthly returns and returns of market index

- Calculate the variance of returns of market index

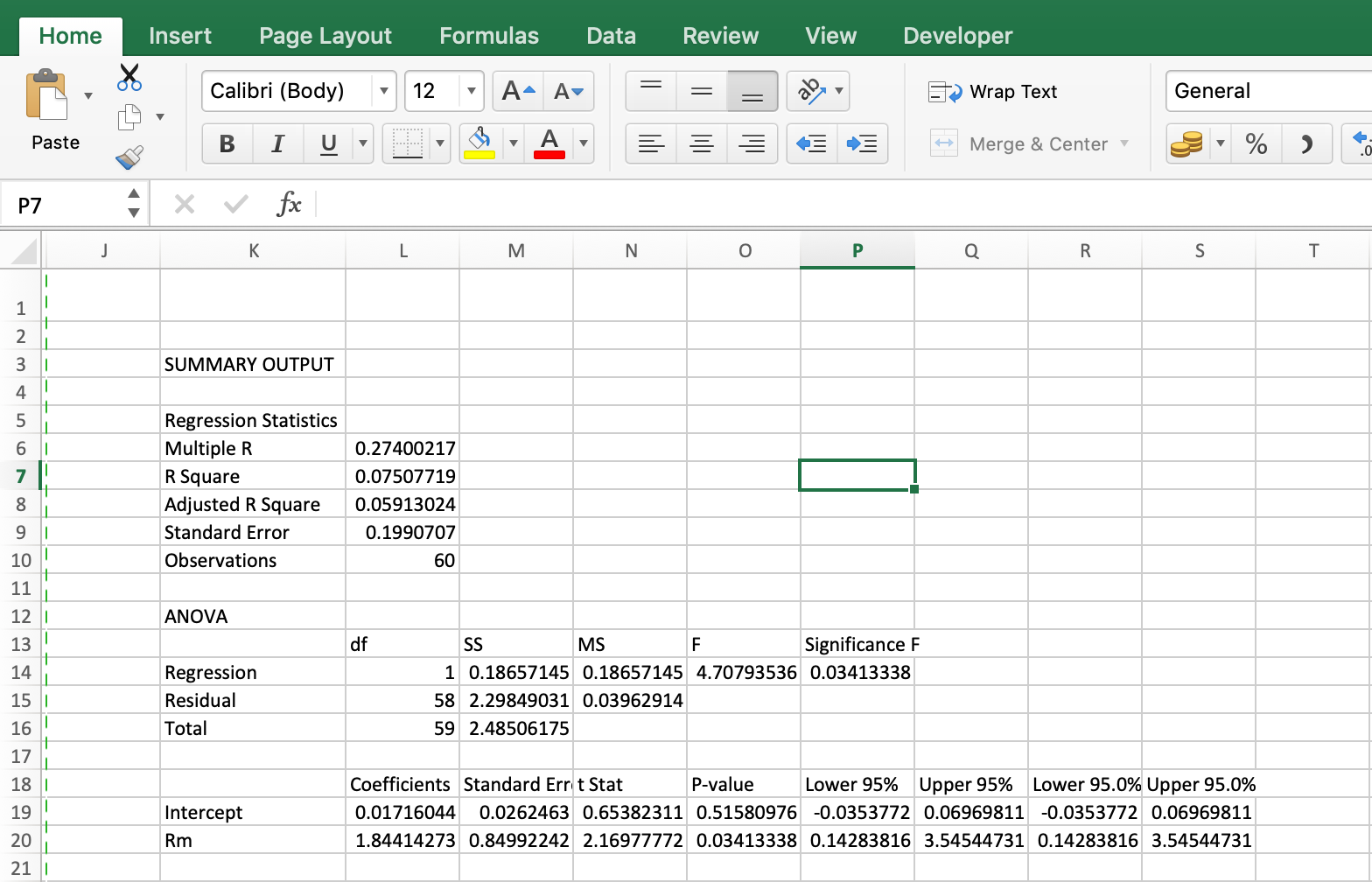

- Or alternatively, Use the linear regression function and select the monthly returns of the market and the stock, each as their own series

- The output from the Linear Regression function is the β

Calculate Using the Formula

Calculate Using Linear Regression

Beta (β) for PT. Medco International Energy

From the calculation of Beta Above, we know that PT. Medco International Energy Beta’s is 1.84. It means that PT. Medco International TbK have High β – A company with a β that’s greater than 1 is more volatile than the market. With β of 1.80 the company would have returned 184% of what the market returns in a given period. (Aji)

Reference:

Gitman, Lawrence J. principles of managerial finance. Tenth edition. Addison-Wesley Longman, Incorporated. 2002.

https://www.investopedia.com/articles/personal-finance/050515/how-calculate-beta-private-company.asp

https://www.investopedia.com/terms/b/beta.asp

https://corporatefinanceinstitute.com/resources/knowledge/valuation/what-is-beta-guide/